Interest rate rise: Bank of England more hopeful on UK economy

The decision to lift rates to 4.25% from 4% came after the inflation rate rose unexpectedly last month.

It also follows the collapse of two US banks and the rescue of Swiss lender Credit Suisse, but the Bank said the UK financial system was "resilient".

The Bank also said the UK was no longer heading into an immediate recession.

"We were really a bit on a knife edge as to whether there would be a recession... but I'm a bit more optimistic now," said Bank governor Andrew Bailey.

However, Mr Bailey warned the UK was "not off to the races", with the economy expected to grow only slightly in the coming months.

Interest rates have been rising steadily in an attempt to tackle rising prices.

Inflation, which is the pace at which prices rise, remains close to its highest level for 40 years at 10.4% in the year to February - more than five times the Bank's target.

The jump in rates means that mortgage costs for some homeowners will rise and some savers could get better returns.

People on typical tracker mortgage deals will pay about £24 more a month following the latest increase and those on standard variable rate mortgages face a £15 jump.

The Bank voted to raise rates after the unexpected rise in inflation last month, but said it still expected the cost of living "to fall sharply over the rest of the year".

It said this was largely due to the government extending energy bill help in the Budget to maintain typical household bills at £2,500 a year, as well as falls to wholesale gas prices.

However, Mr Bailey refused to say whether he thought UK interest rates had reached a peak.

The high price of energy has been the main driver behind the rise in the cost of living over the past year, with gas and oil prices surging in the aftermath of Russia's invasion of Ukraine.

Other factors such as worker shortages and food costs have also fuelled price rises.

The nine members of the Monetary Policy Committee agreed on a to raise rates by a majority of seven to two, with the Bank saying "cost and price pressures have remained elevated".

The Bank noted in its report that there had been "large and volatile moves in global financial markets" since the failure of Silicon Valley Bank in the US and the rescue deal for Credit Suisse, but Mr Bailey said he did not think the turmoil was likely to result in a re-run of the 2008 financial crisis.

In response to the rise in rates, Chancellor Jeremy Hunt said the government supported the decision.

"With rising prices strangling growth and eroding family budgets, the sooner we grip inflation the better for everyone," he said.

But shadow chancellor Rachel Reeves said higher interest rates would cause concern for families.

"The government thinks the cost of living crisis is over, but the reality is that too many families are dealing with a Tory mortgage penalty and battling with soaring food prices," she said.

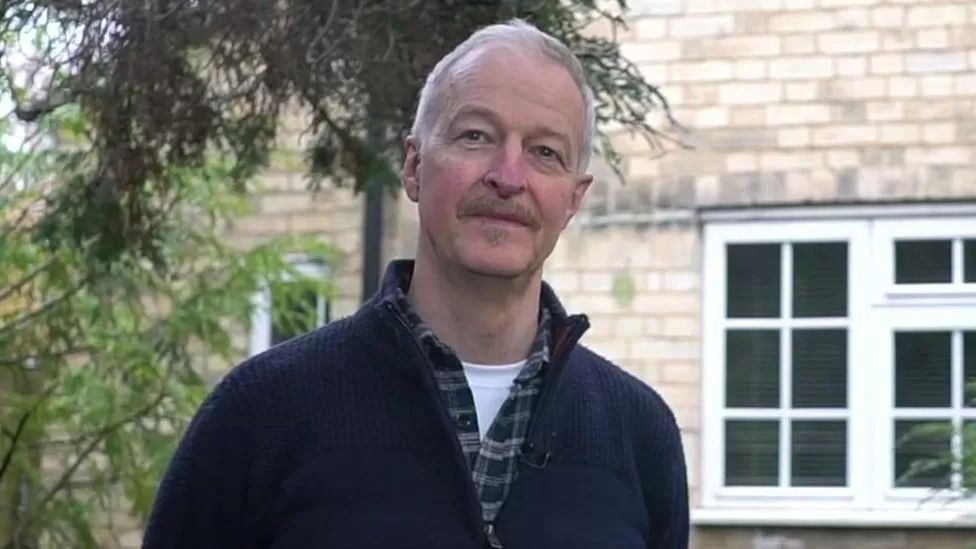

Neil Sutton fears he will have to move

Neil Sutton fears he will have to move

Neil Sutton's monthly mortgage payments were £255 before they started going up in January 2022, but they will rise to £1465 from next month.

"There's not a lot that you can do other than to try and work that much harder to find the extra £150 odd a month. I don't really have an awful lot of choice," he said.

"You know, you just despair, quietly, inwardly, but you know, I can't let that show."

Mr Sutton's 20-year mortgage comes to an end next March and he does not think he will be able to afford to remortgage.

"I guess the bottom line is that we're going to have to move," he added.