The Ledger Will Not Trust on Faith

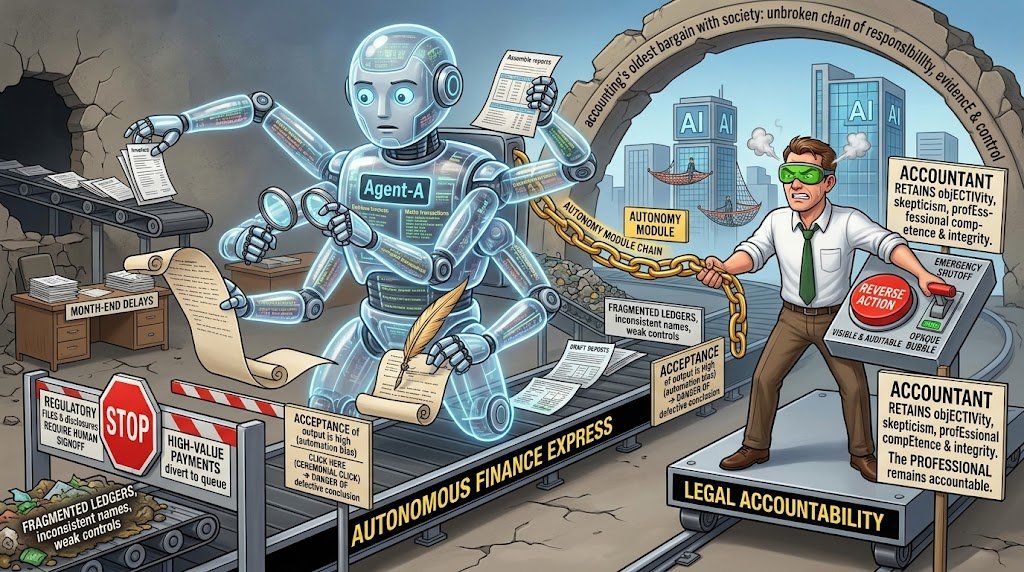

Artificial-intelligence agents can reconcile accounts, pursue anomalies and draft reports, but finance will accept autonomy only when every action remains visible, reversible and humanly accountable.

Trust, rather than computational power, will determine how deeply artificial-intelligence agents enter finance and accounting.

The technology can already perform chains of work that once moved from desk to desk: retrieve invoices, match transactions, investigate discrepancies, prepare journal entries, update forecasts and assemble a draft management report.

The harder question is whether a chief financial officer, auditor or regulator can rely on that work when the machine has acted with limited supervision.

This is a more consequential transition than the arrival of the familiar workplace chatbot.

A chatbot waits for a question and produces an answer.

An agent can be given an objective, decide which systems to consult, choose among several actions and continue until it believes the assignment is complete.

Connected to an enterprise platform, it may read contracts, interrogate ledgers, contact a supplier, recommend a payment or initiate part of a closing process.

The distinction is not semantic.

It separates software that advises from software that acts.

Finance is an unusually demanding place to make that leap.

Its output becomes tax returns, regulatory filings, lending decisions, investor disclosures and audited financial statements.

A polished error can travel farther than an obvious one, particularly when it is repeated automatically across thousands of transactions.

An agent may misread an unusual contract, apply yesterday’s policy to today’s circumstances or retrieve accurate information from the wrong accounting period.

If several agents exchange data or delegate tasks among themselves, reconstructing the path to a mistake becomes harder still.

The attraction is nevertheless substantial.

Agents can monitor accounts continuously rather than waiting for month-end, compare invoices with purchase orders and receipts, identify unusual journal entries, prepare variance explanations and maintain rolling forecasts as new data arrives.

In audit work, they can help examine an entire population of transactions instead of relying chiefly on samples.

In accounts payable, they can chase missing documentation and route exceptions to the appropriate employee.

Tax teams can use them to collect information across jurisdictions and flag inconsistencies before filing deadlines become emergencies.

Much of this remains controlled experimentation rather than unattended autonomy.

Software vendors are embedding agents in finance, accounting and audit products, while large organisations are testing them in bounded processes.

Adoption is advancing faster than governance: one broad enterprise study found that eighty-five per cent of companies intended to deploy agents, but only twenty-one per cent had mature policies for overseeing them.

Another survey found that seventy-eight per cent of executives lacked strong confidence that their organisations could pass an independent artificial-intelligence governance audit within ninety days.

The figures measure executives’ perceptions rather than independently verified compliance, but the mismatch they expose is difficult to dismiss.

The central problem is not whether an agent can produce the correct answer once.

Accounting systems have always contained rules, estimates and automated controls.

The test is whether the result can be reproduced, challenged and assigned to a responsible person.

A dependable financial agent needs a defined mandate, access only to the data required for its task, thresholds beyond which it cannot proceed and a durable record of every consequential step.

It must disclose which information it used, which assumptions it made and where human judgement entered the process.

That architecture turns the abstract language of responsible artificial intelligence into ordinary financial control.

An agent may prepare a journal entry but lack authority to post it.

It may recommend paying an invoice but be unable to alter a supplier’s bank details or approve the transfer.

High-value payments can require two human authorisations.

Unusual transactions can be diverted into an exception queue.

Permissions should expire, sensitive duties should remain separated, and emergency controls should be capable of stopping the system immediately.

Reversibility matters almost as much as accuracy.

Human review, however, cannot become a ceremonial click.

An employee faced with hundreds of machine-generated approvals may develop the same automation bias that already affects other highly computerised work: the tendency to accept an output because the system usually appears competent.

Effective oversight therefore depends on presenting reviewers with the evidence and anomalies that matter, not burying them beneath a transcript of every calculation.

The human must have enough time, expertise and authority to disagree.

Data presents a second obstacle.

Agents do not repair fragmented ledgers, inconsistent supplier names or weak access controls merely by operating above them.

They can accelerate whatever condition already exists.

Clean master data, reconciled systems, explicit retention policies and dependable identity management are consequently prerequisites, not housekeeping to be completed after deployment.

The glamour belongs to the agent; much of the real work remains in the plumbing.

Professional obligations do not migrate to the machine.

Recent international ethical guidance for accountants applies established duties—including integrity, objectivity, professional competence, confidentiality and appropriate scepticism—to emerging technologies.

The practical implication is plain: an accountant cannot defend a defective conclusion simply by pointing to the system that generated it.

The organisation may purchase the model, but the professional remains accountable for how it is selected, constrained and used.

Regulation is developing along the same fault line.

In the European Union, artificial-intelligence systems used for personal creditworthiness assessments and certain life and health insurance decisions are treated as high-risk applications.

Requirements include risk management, technical documentation, logging, accuracy, cybersecurity and human oversight.

Elsewhere, securities and audit authorities are examining how artificial intelligence affects financial reporting, internal controls and audit quality.

Existing duties concerning truthful disclosure, reliable records and professional scepticism continue to apply even when no rule mentions agents by name.

Independence will require particular care in auditing.

An audit firm cannot allow the same opaque machinery to create a company’s accounting position and then appear to test it independently.

Nor can auditors rely on an agent without understanding the data, controls and assumptions governing its work.

Artificial intelligence may widen the auditor’s field of vision, but it does not remove the obligation to obtain sufficient evidence or to challenge management’s estimates.

The profession is therefore likely to embrace agents in stages.

First will come repetitive, high-volume tasks with clear rules and low authority: document collection, reconciliation, classification and anomaly detection.

Drafting and analytical work will follow under visible human review.

Actions capable of moving money, altering the books or shaping a published conclusion will advance more slowly, protected by tighter permissions and explicit approval gates.

This gradualism is not hostility to innovation.

It reflects accounting’s oldest bargain with society.

People accept financial numbers not because every entry is personally inspected, but because responsibility, evidence and control form an unbroken chain behind them.

Artificial-intelligence agents will become part of that chain when they can strengthen it without making accountability disappear inside the machine.

The technology can already perform chains of work that once moved from desk to desk: retrieve invoices, match transactions, investigate discrepancies, prepare journal entries, update forecasts and assemble a draft management report.

The harder question is whether a chief financial officer, auditor or regulator can rely on that work when the machine has acted with limited supervision.

This is a more consequential transition than the arrival of the familiar workplace chatbot.

A chatbot waits for a question and produces an answer.

An agent can be given an objective, decide which systems to consult, choose among several actions and continue until it believes the assignment is complete.

Connected to an enterprise platform, it may read contracts, interrogate ledgers, contact a supplier, recommend a payment or initiate part of a closing process.

The distinction is not semantic.

It separates software that advises from software that acts.

Finance is an unusually demanding place to make that leap.

Its output becomes tax returns, regulatory filings, lending decisions, investor disclosures and audited financial statements.

A polished error can travel farther than an obvious one, particularly when it is repeated automatically across thousands of transactions.

An agent may misread an unusual contract, apply yesterday’s policy to today’s circumstances or retrieve accurate information from the wrong accounting period.

If several agents exchange data or delegate tasks among themselves, reconstructing the path to a mistake becomes harder still.

The attraction is nevertheless substantial.

Agents can monitor accounts continuously rather than waiting for month-end, compare invoices with purchase orders and receipts, identify unusual journal entries, prepare variance explanations and maintain rolling forecasts as new data arrives.

In audit work, they can help examine an entire population of transactions instead of relying chiefly on samples.

In accounts payable, they can chase missing documentation and route exceptions to the appropriate employee.

Tax teams can use them to collect information across jurisdictions and flag inconsistencies before filing deadlines become emergencies.

Much of this remains controlled experimentation rather than unattended autonomy.

Software vendors are embedding agents in finance, accounting and audit products, while large organisations are testing them in bounded processes.

Adoption is advancing faster than governance: one broad enterprise study found that eighty-five per cent of companies intended to deploy agents, but only twenty-one per cent had mature policies for overseeing them.

Another survey found that seventy-eight per cent of executives lacked strong confidence that their organisations could pass an independent artificial-intelligence governance audit within ninety days.

The figures measure executives’ perceptions rather than independently verified compliance, but the mismatch they expose is difficult to dismiss.

The central problem is not whether an agent can produce the correct answer once.

Accounting systems have always contained rules, estimates and automated controls.

The test is whether the result can be reproduced, challenged and assigned to a responsible person.

A dependable financial agent needs a defined mandate, access only to the data required for its task, thresholds beyond which it cannot proceed and a durable record of every consequential step.

It must disclose which information it used, which assumptions it made and where human judgement entered the process.

That architecture turns the abstract language of responsible artificial intelligence into ordinary financial control.

An agent may prepare a journal entry but lack authority to post it.

It may recommend paying an invoice but be unable to alter a supplier’s bank details or approve the transfer.

High-value payments can require two human authorisations.

Unusual transactions can be diverted into an exception queue.

Permissions should expire, sensitive duties should remain separated, and emergency controls should be capable of stopping the system immediately.

Reversibility matters almost as much as accuracy.

Human review, however, cannot become a ceremonial click.

An employee faced with hundreds of machine-generated approvals may develop the same automation bias that already affects other highly computerised work: the tendency to accept an output because the system usually appears competent.

Effective oversight therefore depends on presenting reviewers with the evidence and anomalies that matter, not burying them beneath a transcript of every calculation.

The human must have enough time, expertise and authority to disagree.

Data presents a second obstacle.

Agents do not repair fragmented ledgers, inconsistent supplier names or weak access controls merely by operating above them.

They can accelerate whatever condition already exists.

Clean master data, reconciled systems, explicit retention policies and dependable identity management are consequently prerequisites, not housekeeping to be completed after deployment.

The glamour belongs to the agent; much of the real work remains in the plumbing.

Professional obligations do not migrate to the machine.

Recent international ethical guidance for accountants applies established duties—including integrity, objectivity, professional competence, confidentiality and appropriate scepticism—to emerging technologies.

The practical implication is plain: an accountant cannot defend a defective conclusion simply by pointing to the system that generated it.

The organisation may purchase the model, but the professional remains accountable for how it is selected, constrained and used.

Regulation is developing along the same fault line.

In the European Union, artificial-intelligence systems used for personal creditworthiness assessments and certain life and health insurance decisions are treated as high-risk applications.

Requirements include risk management, technical documentation, logging, accuracy, cybersecurity and human oversight.

Elsewhere, securities and audit authorities are examining how artificial intelligence affects financial reporting, internal controls and audit quality.

Existing duties concerning truthful disclosure, reliable records and professional scepticism continue to apply even when no rule mentions agents by name.

Independence will require particular care in auditing.

An audit firm cannot allow the same opaque machinery to create a company’s accounting position and then appear to test it independently.

Nor can auditors rely on an agent without understanding the data, controls and assumptions governing its work.

Artificial intelligence may widen the auditor’s field of vision, but it does not remove the obligation to obtain sufficient evidence or to challenge management’s estimates.

The profession is therefore likely to embrace agents in stages.

First will come repetitive, high-volume tasks with clear rules and low authority: document collection, reconciliation, classification and anomaly detection.

Drafting and analytical work will follow under visible human review.

Actions capable of moving money, altering the books or shaping a published conclusion will advance more slowly, protected by tighter permissions and explicit approval gates.

This gradualism is not hostility to innovation.

It reflects accounting’s oldest bargain with society.

People accept financial numbers not because every entry is personally inspected, but because responsibility, evidence and control form an unbroken chain behind them.

Artificial-intelligence agents will become part of that chain when they can strengthen it without making accountability disappear inside the machine.